Unexpected travel disruptions can quickly turn a dream vacation into a financial nightmare. From sudden illnesses to airline strikes, unforeseen events can derail even the most meticulously planned trips. This is where travel insurance for trip cancellations and delays becomes invaluable, offering a safety net against significant losses and providing peace of mind for travelers.

Understanding the nuances of these policies is crucial. This guide explores various coverage options, factors influencing premium costs (like trip length, destination, and pre-existing conditions), and the claims process. We’ll also examine how travel insurance interacts with other travel-related services and present real-world scenarios to illustrate its importance. By the end, you’ll be well-equipped to choose the right policy for your next adventure.

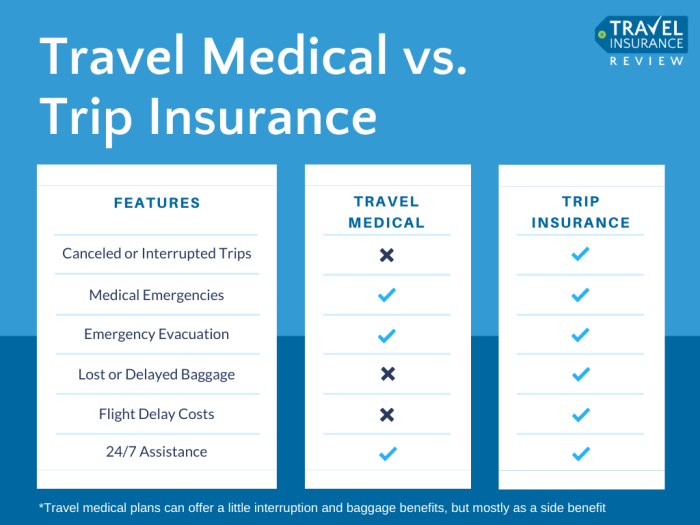

Understanding Trip Cancellation and Delay Insurance

Travel insurance offering coverage for trip cancellations and delays provides crucial financial protection against unforeseen circumstances that can disrupt your travel plans. Understanding the different types of coverage available and the situations they protect against is essential for making an informed decision when purchasing a policy.

Types of Travel Insurance Covering Cancellations and Delays

Several types of travel insurance policies offer varying levels of protection against trip cancellations and delays. Comprehensive travel insurance policies typically include this coverage as a standard feature. However, more specialized policies might focus solely on trip interruption or cancellation. Some policies offer only basic coverage for a limited set of reasons, while others provide more extensive coverage, including reimbursement for non-refundable expenses.

It’s important to carefully review the policy wording to understand the specific events covered.

Causes of Trip Cancellations and Delays Covered by Insurance

Trip cancellation and delay insurance typically covers a range of unforeseen circumstances. Commonly included are medical emergencies (yours or a family member’s), severe weather events, natural disasters, acts of terrorism, and unexpected job loss. Specific policy wording will dictate the exact circumstances covered. For example, some policies might exclude cancellations due to pre-existing medical conditions unless additional coverage is purchased.

Others might have limitations on the amount reimbursed for certain events.

Examples of Beneficial Insurance Use

Imagine you’ve booked a non-refundable family vacation to Europe, and a week before departure, your child falls seriously ill, requiring hospitalization. Trip cancellation insurance would reimburse you for your prepaid, non-refundable travel expenses. Alternatively, consider a business trip delayed due to a sudden volcanic eruption disrupting air travel. Delay insurance could cover additional accommodation costs and other expenses incurred during the unexpected delay.

Another example could be a sudden job loss, preventing you from taking your pre-booked holiday. Again, the appropriate insurance could help mitigate the financial burden.

Comparison of Coverage Levels for Trip Disruptions

Different levels of trip cancellation and delay insurance offer varying degrees of protection. Basic plans might offer limited coverage for a small number of specific reasons, with lower payout limits. Comprehensive plans typically cover a wider range of events, with higher payout caps, and might even include coverage for things like lost baggage or personal liability. The premium cost directly reflects the level of coverage and the extent of the protection offered.

Comparison of Key Features of Various Travel Insurance Plans

| Plan Name | Cancellation Coverage | Delay Coverage | Premium Cost (Example) |

|---|---|---|---|

| Basic Traveler | $5,000 | $500 | $50 |

| Standard Traveler | $10,000 | $1,000 | $100 |

| Comprehensive Traveler | $20,000 | $2,000 | $200 |

(Note

Premium costs are examples only and vary greatly depending on the insurer, trip length, destination, and other factors.)*

Factors Affecting Insurance Premiums

Several factors influence the cost of travel insurance for trip cancellations and delays. Understanding these factors can help travelers choose a policy that offers the right level of coverage at a price that fits their budget. The price you pay is a reflection of the risk the insurance company is taking.Several key elements contribute to the final premium.

These include the length and destination of your trip, your age, and the existence of any pre-existing medical conditions.

Trip Length and Destination

The duration of your trip significantly impacts the premium. Longer trips generally carry a higher risk of unforeseen events, leading to increased premiums. A month-long backpacking trip across Southeast Asia, for example, will naturally cost more to insure than a weekend getaway to a nearby city. Similarly, the destination plays a crucial role. Travel to regions with higher risks of natural disasters, political instability, or health concerns will typically result in more expensive premiums.

A trip to a remote, mountainous region known for unpredictable weather will likely cost more to insure than a trip to a major city in a stable, developed country.

Pre-existing Medical Conditions

Pre-existing medical conditions are a major factor influencing premium costs. Insurance companies assess the potential risk associated with your health history. Individuals with pre-existing conditions that could potentially lead to trip disruptions (e.g., heart conditions, respiratory issues) might face higher premiums or even be denied coverage unless they disclose the condition and the insurer deems it insurable. The severity and stability of the condition will influence the increase in cost.

For example, someone with well-managed type 2 diabetes might see a moderate premium increase, while someone with a recently diagnosed and unstable condition might see a significant increase or face exclusion from coverage.

Age

Age is another significant factor. Generally, older travelers face higher premiums due to a statistically higher risk of medical emergencies. This is not discriminatory; it’s based on actuarial data reflecting the increased likelihood of health issues in older age groups. A 70-year-old traveler will typically pay more for the same level of coverage than a 30-year-old traveler, reflecting the higher potential claims costs for the older age group.

Factors Influencing Premium Cost: A Summary

The cost of your travel insurance is determined by a combination of factors. It’s important to understand how these elements interact to influence the final price.

- Trip Length: Longer trips generally mean higher premiums.

- Destination: Destinations with higher risks (political instability, health concerns, natural disasters) lead to increased costs.

- Pre-existing Medical Conditions: The presence and severity of pre-existing conditions significantly impact premiums.

- Age: Older travelers typically pay higher premiums due to increased health risks.

- Type of Coverage: Comprehensive policies covering a wider range of events (cancellation, medical emergencies, lost luggage) will cost more than basic policies.

- Policy Deductible: Choosing a higher deductible will typically lower the premium.

Claiming Insurance for Trip Disruptions

Successfully navigating a claim for a cancelled or delayed trip involves understanding the process, gathering necessary documentation, and presenting a compelling case to your insurer. This section details the steps involved in filing a claim and offers practical advice to maximize your chances of a successful outcome.Filing a claim for trip disruptions, whether due to cancellation or delay, typically requires prompt action and meticulous record-keeping.

The specific process may vary slightly depending on your insurer, but the core elements remain consistent. A clear understanding of these elements is crucial for a smooth and efficient claims process.

Required Documentation for a Successful Claim

Submitting the correct documentation is paramount for a successful claim. Missing or incomplete documents can significantly delay the process or even lead to claim rejection. Therefore, it’s essential to gather all relevant paperwork as soon as possible after the disruption occurs. This includes your insurance policy, confirmation of your trip booking (flights, accommodation, etc.), proof of the disruption (e.g., cancellation notice from the airline, official weather report), and any expenses incurred as a result of the disruption (e.g., receipts for alternative accommodation, meals).

Examples of Acceptable Proof of Cancellation or Delay

Acceptable proof of cancellation or delay depends on the nature of the disruption. For flight cancellations, an official cancellation notice from the airline, including the reason for cancellation and flight number, is essential. For weather-related delays, a weather report from a reputable source, specifying the severity and duration of the weather event at the relevant location and time, will be required.

For cancellations due to illness, a doctor’s certificate confirming the illness and its impact on travel plans is usually necessary. In cases of unforeseen circumstances like natural disasters, official government reports or news articles verifying the event may suffice.

Tips for Maximizing the Chances of a Successful Claim

Acting promptly is crucial. Contact your insurer immediately after the disruption occurs to report the incident and initiate the claims process. Keep detailed records of all communication with the insurer, including dates, times, and names of individuals contacted. Be honest and accurate in your claim. Provide all the requested documentation in a timely manner.

If possible, gather supporting evidence from other sources, such as witnesses or official statements. Review your policy thoroughly to understand your coverage and the specific requirements for filing a claim. Maintaining clear and concise communication with your insurer will significantly increase your chances of a favorable outcome.

Step-by-Step Guide to Filing a Claim

To ensure a smooth claims process, follow these steps:

- Report the incident promptly: Contact your insurer as soon as possible after the cancellation or delay occurs. Note down the date, time, and the name of the person you spoke to.

- Gather all necessary documentation: Collect all relevant documents, including your insurance policy, trip itinerary, proof of cancellation or delay, and receipts for any additional expenses incurred.

- Complete the claim form: Fill out the claim form accurately and completely, providing all the required information.

- Submit your claim: Submit your completed claim form and all supporting documentation to your insurer as instructed.

- Follow up: If you haven’t heard back from your insurer within a reasonable timeframe, follow up on the status of your claim.

Illustrative Scenarios

Real-world examples highlight the significant benefits of travel insurance, showcasing how it can protect travelers from substantial financial losses and unexpected difficulties. These scenarios illustrate the value of this often-overlooked travel essential.

Scenario: Trip Cancellation Saving Significant Money

Imagine Sarah, a young professional, meticulously planned a two-week backpacking trip across Southeast Asia. She booked flights, accommodation, and various tours, totaling $5,000. A week before her departure, her grandmother, with whom she was very close, unexpectedly fell ill. Sarah had to cancel her trip to be with her family. Fortunately, Sarah had comprehensive travel insurance that covered trip cancellations due to family emergencies.

Her insurer reimbursed her almost the full cost of her prepaid, non-refundable bookings, saving her approximately $4,500. Without insurance, she would have faced a considerable financial burden.

Scenario: Flight Delay Financial Impact

This scenario visually represents the financial impact of a flight delay without travel insurance. Imagine a bar graph. The X-axis represents days of delay, ranging from 0 to 5 days. The Y-axis represents accumulated costs in dollars. For each day of delay, the graph shows increasing costs.

Day 0 shows minimal costs, representing the initial planned expenditure. Day 1 shows an increase, reflecting additional hotel costs for one night. Day 2 shows a further increase, reflecting two nights’ hotel costs plus the cost of additional meals. Day 3, 4, and 5 continue to show a steep rise in costs, incorporating expenses such as additional flights (potentially more expensive last-minute bookings), missed tour bookings, and potential loss of income due to missed work commitments.

The graph clearly demonstrates how costs escalate rapidly with each passing day of delay, with the total cost without insurance significantly exceeding the cost of a travel insurance policy. For instance, a 3-day delay could easily accumulate $1,500 in additional expenses – exceeding the cost of a typical travel insurance policy.

Scenario: Medical Emergency Overseas

Consider John, a middle-aged businessman, who experienced a sudden heart attack while on a business trip to London. He was rushed to a local hospital where he underwent emergency surgery. The medical bills quickly mounted, reaching tens of thousands of dollars. John’s travel insurance covered the substantial medical expenses, including the cost of emergency medical evacuation back to his home country for further treatment and rehabilitation.

The policy also covered the cost of his extended hospital stay and the associated expenses incurred by his family, who flew to London to be by his side. Without travel insurance, John would have faced a catastrophic financial burden, potentially jeopardizing his financial security and future well-being. The insurance provided not only financial relief but also peace of mind during a stressful and life-threatening situation.

Investing in travel insurance for trip cancellations and delays is a smart decision that can safeguard your travel investment. While the cost of a policy might seem like an added expense, the potential savings from covered cancellations or delays often far outweigh the premium. By carefully considering your travel plans and researching different policy options, you can secure the protection you need to enjoy your trip without the worry of unexpected financial burdens.

Remember to always read the policy details carefully before purchasing.

Expert Answers

What types of documentation are typically required when filing a claim?

Commonly required documentation includes flight/cruise itineraries, medical certificates (if applicable), police reports (for theft or accidents), and proof of purchase for non-refundable bookings.

Can I purchase travel insurance after my trip has already begun?

Generally, no. Most travel insurance policies require purchase before your departure date. However, some policies offer limited coverage if purchased after departure, but this is often at a higher cost and with more restrictions.

Does travel insurance cover lost luggage?

Some travel insurance policies include coverage for lost, stolen, or damaged luggage, but the extent of coverage varies. Check your policy details for specifics.

What happens if my claim is denied?

If your claim is denied, you’ll typically receive a detailed explanation of the reasons for denial. You may be able to appeal the decision, but the process and success rate depend on the insurance provider and the specifics of your claim.